9 Min Read

9 Min Read

During our recent trips to Tampa and Miami, we received a few questions about the upcoming cut in the issuance rate of Bitcoin known as the halving. We aren’t forecasters, nor market experts, and don’t pretend to be, but there are some things we can say about it that might help users understand its effect.

What are halvings? (Skip if you know)

Bitcoin has a predetermined rate of issuance instantiated in its source code by its pseudonymous creator Satoshi Nakamoto. This rate of issuance is set to “halve” about every four years and cannot be altered without widespread support throughout the network, which is extremely unlikely to happen given the ideology of its users and developers.

At the genesis of the network, miners were allowed to reward themselves 50 bitcoin for every valid block they mined. This reward amount remained valid for the next 210,000 blocks, or approximately 4 years. In November 2012, the issuance rate was cut in half to a 25 bitcoin reward for every valid block mined. Then in the summer of 2016 the issuance rate was cut again to 12.5 bitcoin for every valid block.

In mid-May 2020, at block 630,000, the rate will be cut in half again to 6.25 bitcoin per block. These halvings will continue until eventually the block reward hits zero over a century from now!

This predetermined halving of new supply fuels a lot of speculation about what it does to bitcoin and the market.

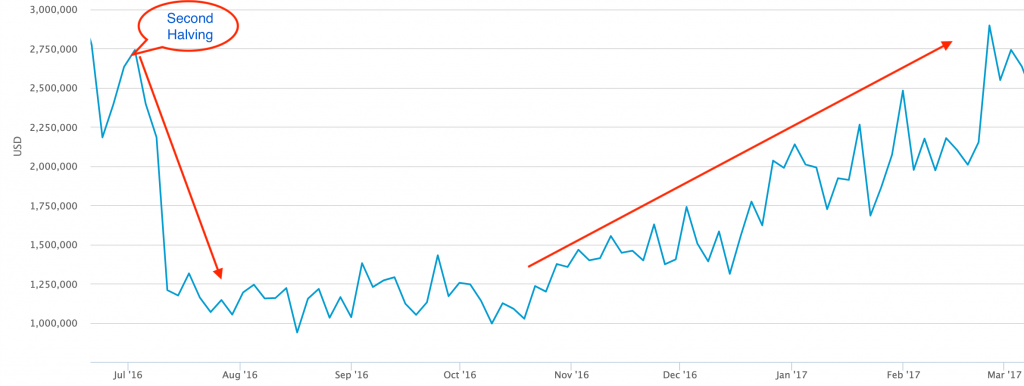

We’ve experienced two bitcoin halvings, and the price increases, although delayed, have been explosive after each halving. The first halving occurred in November 2012, when 1 BTC went for around $11 USD. The following year, the price began to climb dramatically, reaching a new all-time high of over $1,100 in 2013. The second halving, in July 2016, BTC went from around $600 to around $20,000 in 18 months.

Unfortunately, we only have two data points so the empirical evidence to draw from is quite slim. Having only two events isn’t a great base to draw conclusions, but that won’t stop us from talking about it!

Mining

The most immediate and direct effect of the halving has to be on the miners. Their block rewards are cut in half, dramatically reducing their revenue. Low cost miners will be more prepared to weather the reward cut, but some marginal miners that are barely operating at a profit might turn unprofitable rather quickly unless there is a huge increase in fees collected from users or there is a huge price increase that keeps them afloat.

Looking at the history of Bitcoin halvings, this logic seems to bear some fruit, but it’s a mixed bag. After Bitcoin’s first two halvings we see meaningful decreases in mining revenue and hashrate shortly after. In the first halving it took about 2 months for both revenue and hashrate to recovery to pre-halving levels.

1st Halving Mining Revenue & Hashrate:

But in the second halving, the recovery of revenue took much longer than the recovery in hashrate. Hashrate, like before, recovered in 2 months whereas revenue recovered in 8 months as opposed to 2 months in the first halving.

2nd Halving Mining Revenue & Hashrate:

The quick recovery in hashrate coupled with a drag in revenue recovery indicates that a lot of miners either had quite a lot of buffer room to stay profitable, had some savings to work with, became more efficient, were ideologically committed to the project, or had some combination of those four attributes.

If the upcoming halving is anything like the last two, we can expect to see a drop in hashrate post-halving followed by a fairly quick recovery in hashrate. How long it takes for mining revenue to recover after the third halving is harder to ascertain given the wide variance in recovery times.

Reduction in New Supply Hitting Markets

We also know that the cut in the issuance rate cuts the amount of new supply that can be sold by miners. Miners typically have to sell much of their rewards to pay their bills which are mostly denominated and paid for in their local fiat.

If we assume demand for Bitcoin stays roughly constant and there is a reduction of new supply hitting markets, prices should be pushed up. This dynamic should have some effect on markets, but when examining some of the reported volume traded on exchanges compared to the maximum amount of new supply that could be sold by miners, the effect might not be as big as some may wish it to be.

If we use the past six months as an approximate baseline, miner revenue has oscillated between $10 million to $25 million USD a day. We don’t know exactly how much of this is being sold, but we can safely assume that a high percentage of that revenue is sold to cover miners’ operating costs. When we compare the maximum revenue miners can earn to the volumes reported for daily trading, we see miner revenue looks like a relatively small amount.

Over the same six month period, aggregate exchange volumes floated anywhere from $750 million to $5 billion USD worth of BTC per day. These are rough estimates, but this indicates that the ratio of new supply to old supply being traded is quite low. This doesn’t mean cutting the rate of new supply has no effect, it has to and it will, but it may not have as great of an effect as bulls might want it to have. There is still a large overhang of existing supply that can be sold in the market to cancel out any “bullish” effects a cut in the rate of issuance may have. If mining revenue and exchange volume were closer in value, we could expect a halving of new supply to be more impactful. More important than the halving itself is the behavior of those who hold Bitcoin already and those on the outside thinking about moving capital into Bitcoin.

We also have to keep in mind that there are more people and entities in the market that are probably more aware of the halving and have greater ability to express their views in the market than ever before. This might make its effect more muted than previous halvings as the market has become more aware of the effects of the reduction in new supply.

Importantly, the ability to go “short” Bitcoin is easier and more available to participants than ever before. This can help put a top on an overheated market with FOMO buyers crowding in chasing price increases with no regard for the actual value of Bitcoin. Bulls might not like this, but it does help bring about a healthier market with more accurate price discovery. The higher and frothier the top, the harder the fall.

There’s been a long discussion in the Bitcoin community about whether or not the halving itself is “priced in”. Many use the phrase “priced in” to mean that no price gains are available because everyone already knows about the halving. However, a market incorporating information about an upcoming event into its price doesn’t rule out the possibility of potential price increases. The phrase “priced in” only implies participants in and around the market know the information and those participants can and do act according to their views of the information. The halving can be “priced in” and at the same time price appreciation is still very possible. They are not mutually exclusive.

Psychological Effects

The mere existence of halvings and their eventual end attracted a lot of individuals and entities to Bitcoin in the first place and continues to do so.

The creation of a digital token that is provably scarce and is committed to a strict schedule of issuance is “bullish” in the sense that (1) humans have a proclivity for collecting scarce, useful things and (2) Bitcoin exists in a sea of fiat monies, who’s true supplies are generally unknowable, have issuance schedules that are uncertain, and seem to all be going in the opposite direction of Bitcoin. The halvings work to reinforce Bitcoin’s narrative of digital scarcity and remind the market that there will only be so many Bitcoin in the world at any given point in time.

In addition, the halving events attract a lot of attention to Bitcoin which is ultimately a positive for the asset. Like any product or service in the market, the more attention it gets about its properties, the more likely someone hears about it for the first time, learns more about it, and/or interacts with the product or service for the first time.

Because of previous price run-ups after previous halvings, we might be set up for a powerful self-fulfilling prophecy even if the halving wasn’t the proximate cause of the price run-ups. If enough of the market, with enough capital, thinks prices will go up post-halving, they may bid up prices before, during, and even after, trying to get in before a run up in prices. Upward movements in the price attracts even more attention, compounding the effect of the bullish believers and in effect giving more weight to the conclusion that the halvings are bullish for prices.

Financial assets and other luxury goods tend to act in weird ways compared to your typical economic good or service. For most things, as price increases we see a subsequent decrease in demand. For Bitcoin and other goods like jewelry, art, and even education, a higher price often times brings more demand than a lower price would. There are limits to this, but it is a very real effect that’s been observed. Higher prices often times signal higher quality even if it isn’t actually so. And many of the goods and services we buy are used to signal status and wealth and don’t necessarily have much utility for the consumer beyond status or being a part of a trend or fad.

Conclusion: Is the Halving Bullish?!

Historically, absolutely! But unfortunately, the past doesn’t give us full insight into the future. There are a myriad of other factors at play that investors, speculators, and users should consider. It’s hard to conclude that the halving is bullish in of itself, but it is part of a mosaic of attributes that are attractive to a lot of investors and users, including ourselves.

What we can say for sure is the upcoming halving will slow down the rate of dilution for current holders, it’ll generate a lot of media and social media buzz, and marginal miners at the edge of profitability will be affected most acutely. Past that, it’s anyone’s guess!

As a company we think demand for a censorship resistant, inflation resistant, seizure resistant, peer to peer money will continue to increase all over the globe. We’ve been working for years under that assumption, helping make our assumption a reality.

Is Edge bullish on Bitcoin? Absolutely.