6 Min Read

6 Min Read

Decentralized Exchanges, commonly referred to as DEXs, have been operational for years but are still a very small part of the overall exchange market. Much of the exchange market is dominated by centralized exchanges. Decentralization and centralization each serve useful functions for trading cryptoassets. So what’s the distinction between the two type of exchanges?

Decentralization is a prominent buzzword in cryptocurrency and blockchain circles. It’s used to describe almost everything to the point it can lose its meaning and become a fuzzy concept. Many organizations want to latch on to the allure of the term “decentralization” whether or not what they’re offering fits the description.

Although there isn’t a perfect definition of decentralization we try to think of what that definition might be to help us navigate the word-soup thrown at us. In the context of cryptocurrencies and blockchains, we think of decentralization as distributed power and responsibility as well as a distributed physical computing architecture. Perhaps another way of defining decentralization is the absence of a central actor, organization, or structure–either politically, commercially, or technologically. Both descriptions can be useful guideposts for gauging decentralization.

In order to understand decentralization, we first need to understand how centralized exchanges work. There are variations on how centralized exchanges operate but the following is a general outline of how they function:

“Centralized” exchanges are usually run by a for-profit company that takes in and holds customer deposits on behalf of their users. The exchange also controls the market-place for users and matches users based on their orders and preferences.They record orders and buyers are matched with sellers and sellers with buyers, usually in an algorithmic way. The exchange allows users to swap and trade assets on their platform and users have a company hold and exchange on their behalf. Users have to trust that company with their funds and that centralized entity has explicit power and responsibility for the operation of the marketplace.

There are multiple tasks exchanges perform:

- Hold and secure user funds

- Use a private order book and order-matching engine to record orders and match users,

- Settle the exchange of assets

It’s safe to say that if we confronted an architecture that has no central party that is responsible for any of those functions we have a purely decentralized exchange. Or is as decentralized as we could hope for.

Decentralization

So what makes an exchange truly “decentralized”? Does each part have to be decentralized to be considered “decentralized”? What if two of three functions are decentralized, is that sufficient? Or is the presence of one central party enough to contaminate its decentralization? What about one of three? And are all functions equal in their importance or should they be weighted differently? These are all questions up for debate and will be for some time.

And if there is no central entity at the middle of any function the meaning of the word “exchange” changes from business to network.

From our perspective, a decentralized exchange at the very minimum does not have an entity that has access to user funds. At the heart of the issue for most users and the biggest issue with centralized exchanges is their security or lack thereof. A lot of money has been lost on exchanges that have gone bust, been hacked, or were vulnerable to internal corruption. The number one issue every user has is security and the security of their money. People hate losing money!

Minimally decentralized exchanges could more aptly be called non-custodial exchanges. Although not completely decentralized, they are a big step up from centralized exchanges who have complete control of user funds. These non-custodial exchanges, although not holding user funds, still have a lot of power and responsibility over the functioning and maintenance of the exchange. Because of this, these exchanges might have to comply with KYC/AML laws and operators could censor certain coins, users, or regions.

However, there are a few solutions out there that embody the full shift from “exchange” as a platform operated by a company to “exchange” as an active process done on a network where no central entity is responsible for its operation.

Decentralized Exchange(s)

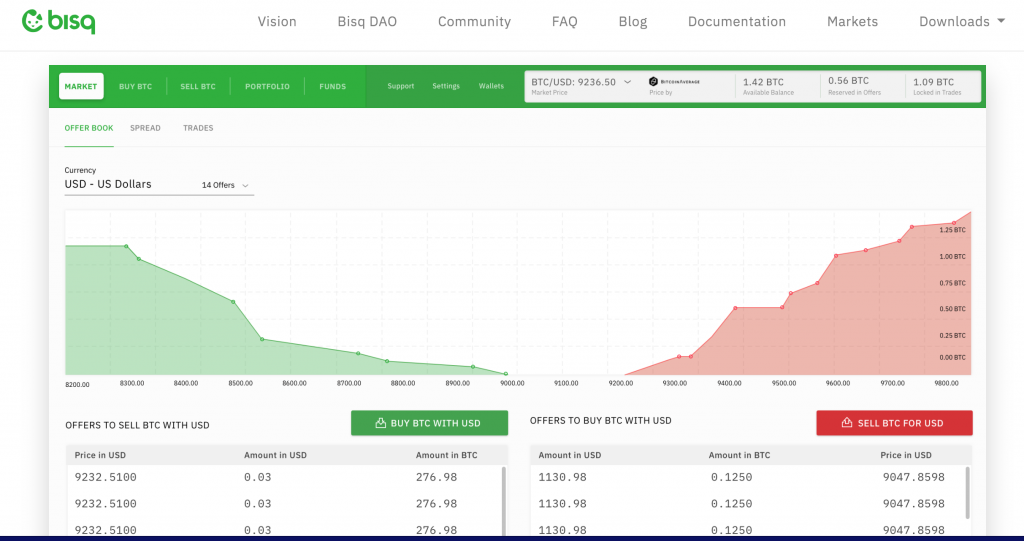

Bisque

Unlike a company like Coinbase, Bisque is not a company but free open source software anyone can run on their desktop. There are no central servers, there is no automatic order matching, and users control their funds. Trades are done on a peer to peer basis. The Bisque exchange uses multi-signature contracts to perform escrow for exchanges between users and uses an arbiter system to handle disputes.

However Bisque and others like it are more difficult to use than their centralized counterparts. Everything is done in a peer to peer fashion so there is no central point of connection that promotes efficiency and ease of use. Users also have to rely on a user based escrow system to handle disputes.

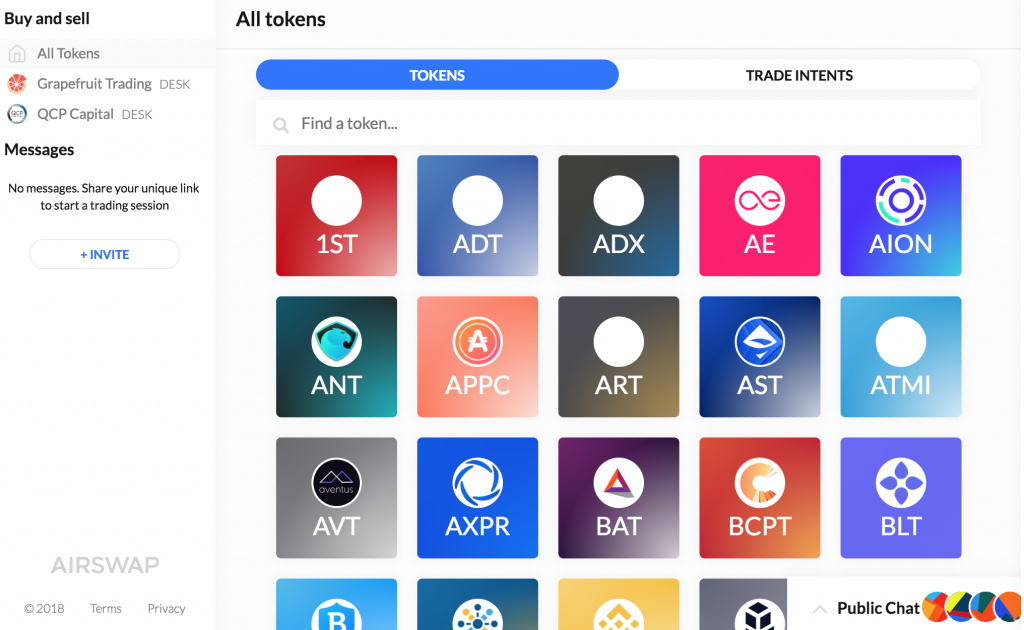

AirSwap

Airswap is a solution built using the Ethereum blockchain that leaves custody, execution, and settlement in the hands of traders. Airswap connects Ethereum wallets to other Ethereum wallets and uses ethereum smart contracts to execute peer to peer trades of ERC-20 tokens. They’ve also developed a peer to peer protocol for order books and order matching.

Right now users can only trade ERC-20 tokens on Airswap. This severely limits the range of possible assets that users could access on other exchanges. Users also have to find their own counterparty to make an exchange.

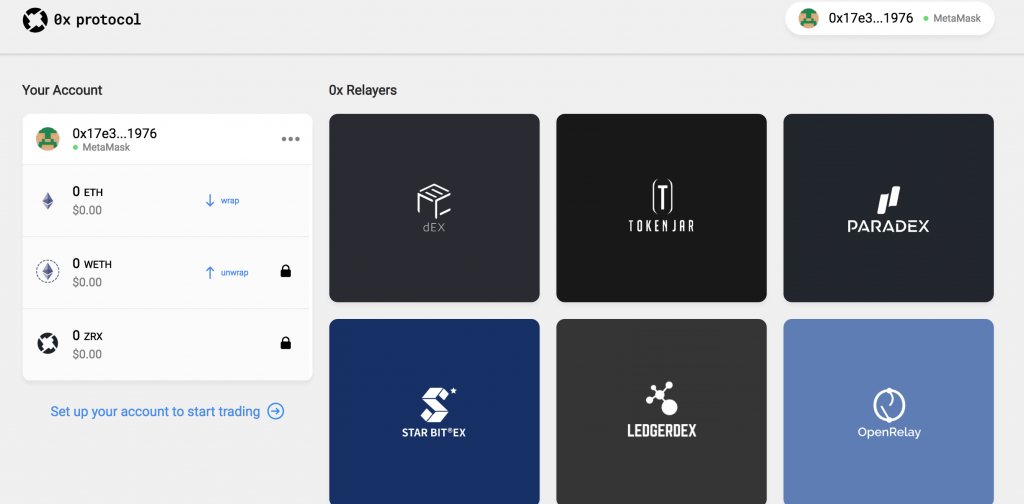

0x

0x is a protocol that allows developers to create their own decentralized exchange on the Ethereum blockchain. These developers build what the protocol calls “relayers” that act as order collecting and matching services. Relayers never hold funds, they are used to connect buyers and sellers essentially running an off-chain order book and matching engine of the protocol. Anyone can become a relayer and even collect fees for their services. The 0x exchange protocol currently only supports the exchange of ERC-20 tokens. 0x also has its own token (ZRX) which is used to pay transaction fees and is used for governance of the protocol.

A decentralized order book removes the possibility that a single entity knows all exchange activity and makes it impossible to censor orders or certain assets from being traded through the 0x protocol.

Unfortunately a decentralized order book makes it possible for sophisticated users and entities to front run other user’s orders. Since the orders are placed on public networks, sophisticated users could use that information to their advantage.

Those peering in on public, decentralized order books and front running orders wouldn’t be doing anything illegal since it isn’t private information. Traders who don’t want to be front-run on decentralized exchanges will have to be sophisticated enough to mask activity that could be used against them. In contrast, those operating centralized order books would be subject to insider trading laws if they got in front of a user’s trade.

Closing Remarks

These options are a few of many solutions being developed to increase the decentralization of exchange. If you’re not a high frequency trader, we recommend at least using non-custodial exchanges which put you at less risk of losing funds and reduces the influence large centralized platforms have on the operation and functioning of the ecosystem.

However, we should also acknowledge that decentralization isn’t necessarily important nor effective in all situations or contexts. Centralization and decentralization each have their benefits and trade-offs. Because of unavoidable trade-offs we expect to see a diverse ecosystem of trades taking place on centralized services and growing network(s) of decentralized exchange.