11 Min Read

11 Min Read

There’s been a lot of commotion surrounding the Federal Reserve, the US Treasury, and financial markets given the recent volatility in the stock and credit markets , tweets by President Donald Trump, and impromptu calls to the six largest commercial banks in the United States from the Secretary of the US Treasury .

The events of the last few weeks serve as a good reminder about how the US financial system works and adds context to the environment crypto-assets are nested in.

Brief Monetary History of the United States

The founding of the United States and the subsequent 19th century saw a mish-mash of different monetary schemes across a patchwork of state banks, national banks, and sometimes a Central Bank. Despite the different schemes, throughout most of the 19th century dollars, bank notes, and other liquid assets issued by commercial banks or a central bank were backed by metal coins made from gold or silver. During the War of 1812 and the Civil War, redemption of gold and silver was suspended giving the US government more flexibility in its ability to finance its war efforts.

The United States started the 19th Century with a financial system dominated by state chartered banks and a central bank which connected state banks, the newly formed US government, and international capital. However, the first iterations of central banking in the United States were much different than the Federal Reserve system we are familiar with today but generated similar controversy and distrust. From the start, central banking in the United States had many enemies. One of those enemies, Andrew Jackson, became President of the United States in the early 1830s hoping to kill America’s central bank. He wasn’t able to destroy it but he refused to renew its charter in 1836.

After 1836 the era of “free banking” reigned supreme with no central bank in the middle of the financial system. A decentralized system of state chartered banks dominated US finance and money creation. It wasn’t until after the Civil War that national banks formed under the charter of the US government who worked to create a national banking system and a single currency unit that tied the previous free banking system together into a national system.

After a 77 year break (1837-1913), central banking in the United States returned with the passage of the Federal Reserve Act which created the Federal Reserve system we have today. Major changes to how central banking is conducted have been made since the Fed’s inception.

The most consequential changes in the international financial system since the Fed’s birth revolved around the shifting global political order and the switching on and off of some form of gold standard. Finally in 1971, President Nixon put an end to an already beleaguered and bruised gold standard by ending the US dollar’s international convertibility into gold. This officially ended the US dollar’s peg to gold and started the beginning of a purely fiat global financial system.

The Federal Reserve Notes carried around in people’s pockets and held in reserves at commercial banks are not backed by precious metals such as gold or silver. These notes are backed by US Treasury securities held by the Federal Reserve. In essence, Federal Reserve Notes are backed by the faith of financial markets, the international community, and US citizens in the US government’s ability to stay true to its obligations. Since the US Government is reliant on the tax receipts of its subjects to stay true to its obligations, arguably the assets of the US taxpayer are the collateral for the Federal Reserve system post 1971. The events of the 2008 financial crisis seem to confirm that relationship.

Money (credit) Creation in the Federal Reserve System

The Federal Reserve system is a public-private partnership between the US Congress, the US Executive, and nationally chartered commercial banks in the United States. Congress gave the power to conduct monetary policy to the Federal Reserve with certain mandates, the President appoints high level officers to the Federal Reserve, and member banks vote on high level staff, store reserves, and have ownership stakes in the institution. The system functions through a complex set of relationships between federal power and financial power that isn’t purely private or public.

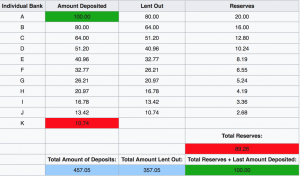

The Federal Reserve system is a fractional reserve banking system meaning multiple claims can be made on a single deposit. A nationally chartered bank only has to hold a small percentage of demand accounts and is allowed to loan out the rest. This process of fractional reserve lending leads to something commonly known as the money multiplier effect which is the primary driver of money creation in this system. The chart below shows the money multiplier effect, assuming the reserve requirement is 20%.

What we see is that out of just $100 deposited by a bank customer a fractional reserve system is able to create an additional $357! However, of the total amount shown to bank customers only 20% of that actually exists. The additional $357 only exists as long as enough of the users of this system don’t try to redeem their entire balance at the same time.

To become a money creator of this sort in the Federal Reserve System, an institution would have to be chartered by the Office of the Comptroller of the Currency. We could call this “Proof of Authority” instead of “Proof of Work”. Nationally chartered commercial banks are the primary driver of money (credit) creation in the Federal Reserve system.

Keep in mind the word “money” in the context of the Federal Reserve system could be interchanged with the word “credit” or “debt” without much problem. This is why throughout this post I add (credit) alongside the word money. The equivalency of money and credit is quite odd for those immersed in the world of digital assets which are most similar to commodity monies like gold and silver.

Although the member commercial banks are the main driver of money creation, the Federal Reserve has some powerful indirect and direct tools to affect the supply and demand of money (credit). These tools include reserve requirements, a discount window, and a target rate.

Reserve requirements detail the percentage commercial banks must keep in reserve as non-loanable funds. The discount window acts as the Fed’s lender of last resort mechanism and allows member banks to borrow directly from the Federal Reserve extremely cheaply during liquidity shortages or what other businesses call bankruptcy. And lastly the most publicized, and indirect tool is known as the federal funds target rate. This rate is what all the press hubbub and presidential tweets have revolved around recently. The target rate is set by a group at the Federal Reserve called the Federal Open Market Committee (FOMC).

This rate targets the federal funds rate which is the rate depository institutions at the Federal Reserve lend reserve balances to each other overnight. The target rate set by the Fed tries to influence the effective interbank lending rate between institutions to meet broad financial and economic goals determined by the Federal Reserve and its legislative mandates. If the Fed thinks the effective rate is too high or too low they will conduct what they call open market operations (buying and selling of US Treasuries) to bring the interbank rate or federal funds rate into the range they want to see given their interpretation of economic and financial conditions.

Powell, Rates, and Trump

The current FOMC headed by Federal Reserve Chairman, Jerome Powell, have been gradually raising the target fed funds rate which had been at the lowest levels in its history for almost a decade. Powell and the other members on the FOMC have decided to engage in open market operations that pulls supply out of circulation pushing the price of credit up. Previous Fed Chairs, Ben Bernanke and Janet Yellen, aggressively lowered the target rate and kept it at near 0 to keep the supply of cheap credit flowing during and after the 2008 financial crisis.

Powell, who was appointed under Trump, has been making it slightly more expensive to create money or obtain credit in the Federal Reserve system. President Trump has been vocalizing his disagreement because the rising price of credit can put the breaks on an economy and financial system that is dependent on cheap credit. Many US corporations, the real estate market, the auto market, the bond market, and the stock market are all reliant on cheap credit flowing.

Powell and his crew at the Federal Reserve point to a strong labor market, decent economic growth, stable inflation, and the need to unwind the Fed’s huge balance sheet as the reasons for hiking the target rate. Financial markets and the economy in general have been operating for over a decade on a cheap and artificial input. One could see why this would have a negative impact on activity that is highly dependent on the cheap input.

If a business or market is highly dependent on the price of oil being cheap, high oil prices will negatively impact that business or market. The same phenomena is happening to financial institutions, markets, and other economic activity that depend too much on cheap credit.

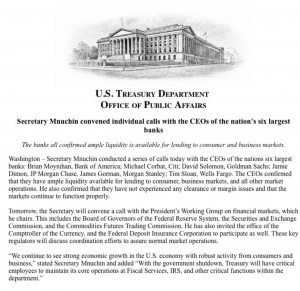

Mnuchin & the Big Six

On December 23rd 2018 the Secretary of the Treasury Steve Mnuchin put a call in to the CEOs of the nation’s six largest commercial banks: JP Morgan, Wells Fargo, Goldman Sachs, Bank of America, Citi, and Morgan Stanley. The CEOs assured the Secretary that they had “ample liquidity to lend to consumer, business markets, and all other market operations”.

Why was this done? It’s hard to know but from the outside looking in it seems analogous to a situation in which a friend of yours texts you out of the blue and assures you everything is alright and assures you there is nothing to worry about without you asking them or being aware that you should worry. This isn’t very comforting and at the very least suspicious but there isn’t much about the move that leaves room for a definitive conclusion about the financial health of these banks.

However, the actions of the Secretary of the Treasury show that the US financial system is dependent on the health of only six commercial banks who have to manage and operate a system built on fractional reserve lending (multiple claims on the same underlying assets) within a web of interbank promises and US government IOUs which are ultimately backed by the assets of the US taxpayer. Thats an extremely tough task, one could say an impossible task to be managed by so few.

If too many claims are made simultaneously on the same underlying assets, the system seizes up unable to redeem all the claims causing inter-bank trust and lending to crater. The flow of credit then grinds to a halt which disrupts economic activity and financial markets because of the system’s dependence on inter bank trust and readily available, cheap credit. The US taxpayer, being the collateral in this system, will be called upon again to provide “ample liquidity” to the too-big to fail banks in order to save the system. We’ve seen this movie before.

Bitcoin & “Crypto”

Satoshi famously included this text in the the genesis block: “The Times 03/Jan/2009 Chancellor on brink of second bailout for banks” referring to the bailouts happening in the UK at the same time the Bitcoin project became operational.

In the Bitcoin architecture and the designs of the other crypto-assets it inspired, there is no central administrator, there is no haggling about interest rates or price controls, there are no lenders of last resort, there are no government charters, and there are no institutions that are too big to fail. The protocols, projects, and businesses in crypto survive, thrive, or die on their own merit.

Going into 2019, Bitcoin and the larger crypto-asset ecosystem is in a great position to compete for the trust and use of billions of people across the planet. Many have had no choice but to use financial markets and infrastructure dominated by first world central banks like the Federal Reserve who act as the final backstop for a small number of first world fractional reserve commercial banks. The sad part is, people in developing countries usually have a much less trustworthy and functional financial system than their more fortunate developed counterparts. The developed world’s financial system is the best looking house in a horrendously ugly neighborhood.

Now, thanks to the efforts of Satoshi and many others, people have more financial choices and we at Edge are here to help users all around the world engage with these new financial protocols in a secure, private, and easy to use way. Opting out of the centrally managed-debt based-fractional reserve banking system has never been easier.